Important Updates to Consider as Part of Your Retirement Plan

Key Takeaways

- Every year, the IRS adjusts retirement plan contribution limits for inflation.

- Increases in contribution limits allow you to save more in tax-advantaged accounts, such as your 401(k), IRA, and Health Savings Account.

- If you didn’t save as much as you’d hoped in 2025, you have until your tax filing deadline to catch up on IRA contributions.

Retirement preparedness plays a central role in long-term financial planning, whether you are actively building toward retirement or just beginning to consider your options. The Internal Revenue Service (IRS) provides opportunities to support retirement savings through tax-advantaged accounts, including 401(k) plans, IRAs and Health Savings Accounts (HSA).

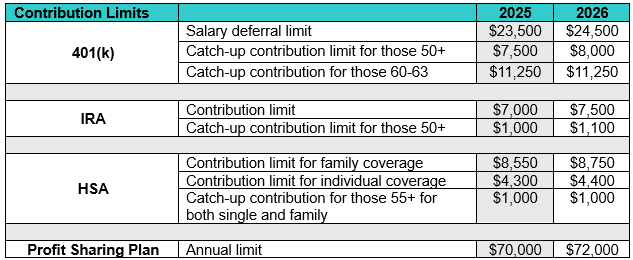

For 2026, the IRS has increased the contribution limits for these accounts and adjusted related income thresholds as part of its annual cost-of-living updates. Key changes are listed below. For more details, refer to Notice 2025-67.

Key Changes for 2026

- 401(k) salary deferral limit increases to $24,500 per individual 401(k)

- 401(k) catch-up contributions at $8,000 for those 50 and over

- IRA contribution limit at $7,500 and the additional catch-up contribution limit for individuals aged 50 and over at $1,100

- HSA contribution limit increased to $8,750 for family coverage and $4,400 for individual coverage

- Profit Sharing Plan annual limit increased to $72,000

Stayed the Same

- 401(k) catch-up contribution for individuals aged 60-63 in 2026 is $11,250

- HSA catch-up contributions at $1,000 for those 55 and over for both single and family

Income Phase-Out Ranges

Taxpayers can deduct contributions to a traditional or Roth IRA if they meet certain conditions. If during the year, either the taxpayer or the taxpayer’s spouse is covered by a retirement plan at work, the deduction may be reduced, or phased out, until it’s eliminated, depending on filing status and income.

In 2026, the income ranges for determining eligibility to make deductible contributions to a traditional or Roth IRA are increasing.

The adjusted gross income (AGI) phase-out range for taxpayers making contributions to a traditional IRA covered by a workplace retirement plan is $129,000 to $149,000 for married couples filing jointly. For singles and head of households, the income phase-out range is $81,000 to $91,000.

The Roth IRA phase-out range is $242,000 to $246,000 for married couples filing jointly. For singles and head of households, the income phase-out range is $153,000 to $168,000.

If you earn too much to open a Roth IRA, you can open a nondeductible IRA and convert it to a Roth IRA. This is known as the Roth “Back Door” strategy.

Estate and Gift Tax Thresholds

The federal estate tax exclusion amount—how much an individual can shelter from estate taxes—is $15 million for deaths in 2026, up from $13.99 million in 2025. Individuals can make lifetime gifts, outright or in irrevocable trusts, up to that amount without incurring federal estate or gift tax. The giver owes tax only if the amount goes over the threshold. Listen to this Accumulating Wealth Podcast episode to learn more about preparing your estate plan.

A separate limit on tax-free gifts remains at $19,000 for 2026. These gifts don’t count toward the lifetime maximum, and neither the gift giver nor receiver is taxed.

Catching up on 2025 IRA Contributions

If you paused your normal contributions or didn’t save as much as you’d hoped, it’s not too late to catch up on your 2025 savings. You have until April 15, 2026, to make 2025 IRA contributions. The deadline is Oct. 15, 2026, if you’re filing with an extension.

If you exceeded the 2025 IRA contribution limit, you may withdraw excess contributions and any income earned on those excess contributions from your account by the due date of your tax return (including extensions) to avoid penalties. If you do not, you must pay a 6% excise tax on the excess amount for each year it remains in your account.

Looking Ahead

The Tax Cuts and Jobs Act (TCJA) provisions for individual income tax rates and the standard deduction were originally set to expire after 2025. However, the One Big Beautiful Bill Act (OBBBA), enacted in July 2025, made most of these provisions permanent with some modifications. For tax years beginning in 2025, the individual income tax rate brackets remain at 10%, 12%, 22%, 24%, 32%, 35% and 37%—these rates do not increase due to the TCJA sunset. The increased basic standard deduction amounts are made permanent and will not decrease beginning after 2025. Also, the amounts are increased for 2025 to $31,500 for married filing jointly, $23,625 for head of household, and $15,750 for single and married filing separately.

Under OBBBA, the SALT deduction limit for individuals who itemize deductions is temporarily increased for tax years 2025 through 2029. The limit is $40,000 ($20,000 if married filing separately) for 2025, $40,400 ($20,200) for 2026, and increases by one percent over the previous year’s amount in 2027 through 2029. The dollar limit for 2025 through 2029 is reduced by 30 percent of the excess (if any) of the taxpayer’s modified AGI over a threshold amount but not below $10,000 ($5,000 if filing separately). In addition, for tax years beginning in 2026, an individual who does not itemize deductions can deduct up to $1,000 ($2,000 in the case of a joint return) in charitable contributions made in cash during the tax year.

OBBBA permanently increases the estate, gift and generation-skipping transfer GST exemption to $15 million per person starting Jan. 1, 2026, indexed for inflation—and this new amount does not sunset unless Congress passes a future change.

Accumulating Wealth Podcast Episode 208

For a deeper dive into these and other contribution limit changes, don’t miss hosts Hunter Satterfield and Judson Crawford in this episode of the Accumulating Wealth Podcast.

Looking to ensure you take advantage of the limits as they apply to you? For a complimentary consultation, reach out to our team.